If you want to win with money, you’ve got to change your actions with money. The way you do that is by making a budget and sticking to it. And the way you do that is by tracking your expenses.

This is the secret to taking your budget from good intentions to awesome outcomes. So, let’s talk about how to track your expenses in four steps—plus why it’s so important anyway.

Steps to Track Your Expenses

Tracking your expenses (aka tracking your transactions) isn’t hard—it’s a habit. And just like other important habits—you know, like flossing—it takes some work and repetition to go from trying to remember to do it to doing it naturally. But you’ll get there. And your teeth and budget will thank you. Just follow these four steps.

Step One: Create a Budget

You won’t be able to track expenses without one. What’s a budget? It’s your monthly money plan where you’ll give every dollar that comes in during the month a job to do, whether that’s spending, saving or giving.

And listen, budgets get a bad rap. Has anyone ever told you a budget is too limiting? The truth is, a budget doesn’t control you—you control it. It’s a guide you set up to make sure your money does what you tell it to do. So, it actually gives you permission to spend!

And here’s how you go about setting up a budget:

1. List your income.

List out each paycheck coming this month. (Don’t forget any extras like that side hustle!) Add that all up. This is how much money you have to work with this month!

Got an irregular income? Just look back at what you’ve made the last few months. List the lowest amount as this month’s planned income. We’ll talk more about this in a moment.

2. List your expenses.

Time to plan for everything you’re paying for this month. List your expenses in this order:

- Giving (10% of your income)

- Savings (depending on your Baby Step)

- Four Walls (food, utilities, shelter/housing and transportation)

- Other essentials (insurance, debt, childcare, etc.)

- Extras (entertainment, restaurants, etc.)

3. Subtract your expenses from your income.

This should equal zero. If you’ve got money left over, that’s awesome! Put it toward your current Baby Step (the proven, guided path to saving, paying off debt, and building wealth). If you’ve got a negative number, lower your planned totals or cut extras until you get zero.

This is called zero-based budgeting, and, as we said before, it’s all about giving every single dollar you make a job to do. That way it works as hard as you do.

Now that you’ve set up your budget, you’ve got to keep up with it. That’s where the tracking comes in!

Step Two: If You Make Money, Track It

When your regular paycheck comes in, put it in the income part of your budget. If you make money through a side hustle or sell something, log that in too!

This step is super important if you have an irregular income. Remember, you planned low when you listed your income. So, if your income turns out to be more than you planned, now’s the time to adjust. You can add money to your current budget lines or cover some extras in the budget.

Even with a regular income, track it! For one, you can make sure nothing’s off with your paycheck. For two, it’s another way to get you in your budget (which is always a solid win).

Step Three: If You Spend Money, Track It

Track every single expense you make. All month long.

Start budgeting with EveryDollar today!

When you fill up the gas tank, subtract that expense from your transportation budget line. When you pay the rent, subtract that expense from your housing line. When you buy tickets to see your fave boy band’s reunion tour, subtract that expense from entertainment.

You get the picture. If money’s coming out of your wallet, bank account, PayPal, cash envelope, coin purse or old-fashioned piggy bank—track it.

As you’re tracking, make sure you’re subtracting too. Then you can see how much you have left in your different budget categories. This is where the magic happens—because this is where you’re keeping up with spending to keep from overspending!

Step Four: Set a Regular Rhythm for Tracking

Track your expenses regularly. That might be once a week or at the end of each day—or it might be before you leave the grocery store parking lot.

Whatever works for you and gets every expense tracked with no paper receipts getting lost in that kitchen drawer that must be some kind of portal to another world. (How else do you explain the things that go in but never come out?)

If you’re married, make sure both of you are working from the same budget and tracking expenses. This is great for accountability and communication. That way, neither one of you will ever say, “I didn’t know you spent most of the entertainment budget on ziplining tickets. I wanted to sign us up for a couples hip-hop dance class.”

Quick Callout: If you upgrade to the premium version of EveryDollar, tracking is a breeze. You can connect your budget to your bank, so transactions automatically stream in. You just drag and drop them to the right budget line. Boom.

Why Should You Track Your Expenses?

We just touched on this, but now we’re going deeper. Because, let’s be honest, if all you’re doing at the start of each month is jotting down planned budget lines, you aren’t holding yourself accountable to keep within those lines.

Many of us began “budgeting” this way. And it’s a start. It’s good to have an impression of what money should go where. But if you aren’t tracking your expenses, you don’t know where your money is really going. You’ll run the risk of continually setting unrealistic budgets, and you’ll never meet your money goals.

And that isn’t what we want for you. We want you to succeed. Times ten! So, let’s look at different methods to make that happen.

Four Ways to Track Your Expenses

1. Pencil and Paper

Don’t dismiss old school methods. Plenty of people stick to a paper budget as their money tracker method.

Pro: The biggest benefit here (besides not needing access to technology) is that physically writing things down requires an active brain. And active brains are really helpful when you’re dealing with money.

Con: The downside to this method is pretty clear: Most of us don’t keep up with paper copies of stuff these days. Sometimes you misplace receipts (or lose them in that portal kitchen drawer). Or forget the cash you spent on a quick trip to the dollar store. Or don’t write down a couple debit card purchases.

Any of these communication breakdowns (with yourself or your spouse) can lead to a busted budget.

Conclusion: Hey, budgeting with pencil and paper is way better than no budget at all. If it’s the only way you want to go, then go for it! Also, if you want to start out on a paper budget and then move on to some other method, check out our Quick Start Budget.

2. Envelope System

The envelope system focuses on paying cash for as many things in the budget as you can. You can auto draft things like retirement, mortgage and some utilities, and you might send checks or make a debit card payment online for other bills. But you’ll stick to cash for all the expenses you pay for in person.

At the start of the month, you put cash in envelopes (or use a special divided wallet) labeled with your budget lines. Groceries, entertainment and restaurants are three great examples.

Pro: With the envelope system as your expense tracker method, you know exactly when to cut back on spending, because you see when the envelope starts getting low. And when the envelope is empty, you’re done spending. Your money is essentially tracking itself.

Con: Let’s face it, though, paying in cash can sometimes be inconvenient. Plus, with the rise of e-commerce, paying cash isn’t always an option.

Conclusion: Even with its cons, this is a powerful way to track expenses, because physically watching the money leave the envelope inspires a whole new level of responsibility. In fact, even if you go with a different method for tracking your expenses, doing the envelope system with some of your budget lines is a great way to manage your money.

3. Computer Spreadsheets

It’s time to talk digital—computer spreadsheets as an expense tracking method.

Pro: Plenty of people are spreadsheet fanatics, and they’ll talk to you about its perks until the end of time. The tons of templates, the ability to customize your budget, the beauty of having the math done for you on the screen—these are a few benefits to spreadsheet budgets.

Con: One problem with this method is that those spreadsheet enthusiasts aren’t always married to fellow spreadsheet enthusiasts. Couples should be in open communication about their spending. Don’t let spreadsheets come between your happily ever after!

The second disadvantage to spreadsheets is physically getting to your computer to keep up with your spending. If you aren’t making regular visits to enter expenses, your budget isn’t really a budget—it’s just a spreadsheet full of plans. Laying out the plan is where you start, but plans without follow-through don’t accomplish goals.

Conclusion: Again, if spreadsheets are the only way you want to budget and handle your expense tracking, that’s better than skipping budgeting completely!

And here’s the thing, computer spreadsheets aren’t the worst or anything. But you know what’s always by your side? Your phone. Which brings us to the next—and, we boldly declare, best—option for tracking your expenses. Drum roll, please.

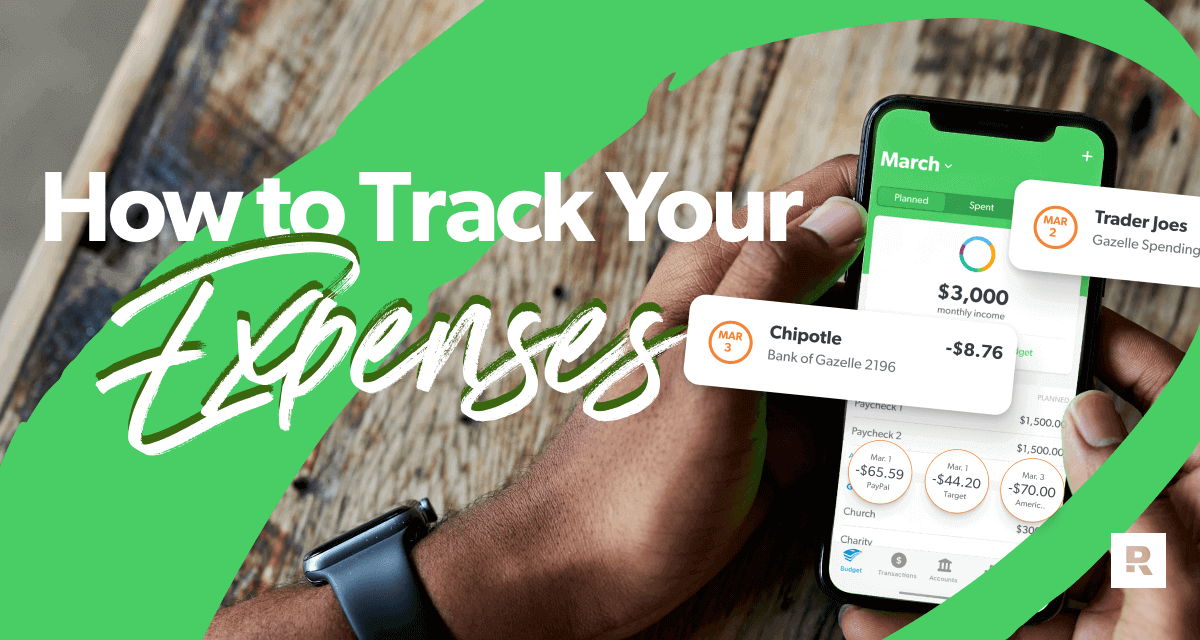

4. Budgeting Apps

Specifically, EveryDollar. We’re not going to beat around the bush here. With our free budget app, you can create an on-the-go budget and literally change your financial life.

Pro: You can log in on your phone and track the expenses moments after they show up on your bank account. Don’t leave the parking lot of the dollar store without recording that you spent $3 and tax on a birthday balloon, gift bag and stuffed clownfish you hope your toddler niece will think is Nemo.

As you can see, the convenience of a budgeting app is its greatest asset. Of course, EveryDollar boasts even more. Customize your templates to make them fit your spending and saving needs. Set up funds to meet big money goals. And you can turn two budgets into one with your spouse when you sync both of your devices to one EveryDollar account.

And remember, upgrading to get the premium version of EveryDollar automatically streams your expenses right into your budget. No remembering receipts. No mistyped math. No secret spending. That brings ease, accuracy and accountability to your budgeting game. Win. Win. Win.

Con: The key thing to remember is this: You can’t set up your budget and leave it (but that’s true of any budgeting method). The app doesn’t shut down your bank account when you’re about to buy a 17-layer burrito that’ll push your restaurant budget over the edge. The only con with a budgeting app is that you still have to be in the habit of tracking those expenses.

Conclusion: If you aren’t watching where your money is going, you’ll always wonder where it went. But when you set yourself up with the right tool (aka EveryDollar, our fave expense tracker) and know the work is worth it (which we totally verify from personal experience), you’ll move beyond good intentions into financial victories.

Get an Expense Tracker and Track Your Expenses (Every Single One)

Okay. You’ve seen the why and the how and the popular methods for money tracking. Now it’s time to get on it. Download EveryDollar and make it easy to create a habit out of tracking your expenses (every single one).

There you go! That’s the secret to budgeting well. And now that it’s not a secret, you can make it happen!

Did you find this article helpful? Share it!

About the author

Ramsey