How Much House Can I Afford?

13 Min Read | Oct 17, 2023

Listen to this article

Buying a house. It’s a huge life milestone and comes with a lot of emotions. (Excitement? Check. Slight panic? Also check!) But don’t worry. I want to show you how our home affordability calculator can help you figure out how much you should spend on a house.

I want you to feel confident about how much house you can afford before you hit the ground running and start shopping. And our How Much House Can I Afford? calculator can do just that. All you have to do is enter your monthly income into our home-buying calculator to instantly get a home price that fits your budget.

Did you give it a whirl? As you can see from the results, how much house you can afford really depends on the relationship between your income and the mortgage.

Now, this calculator is going to give you a pretty close number for how much house you can afford, but you’ll need to factor in mortgage values specific to the market you’re looking to buy in before you make a final decision. A RamseyTrusted real estate pro can help you do just that.

To figure out how much mortgage you can afford with your income, housing lenders use different guidelines—but most lenders dish out mortgages that are way more than people can afford . . . and keep them in debt for decades longer than they have to be!

I want you to buy a home that’s a blessing, not a burden. And the only way to do that is to understand your home-buying budget and stick to it!

That’s where our home purchase calculator comes in. How does it work? Let’s do a little math and see.

How to Calculate How Much House You Can Afford

To figure out how much house you can afford, all you need to do is crunch a few numbers. If math isn’t your thing, hang in there. I’ll walk you through it step by step. (I’ve never lost a patient!)

And for you married folks, make sure you and your spouse look at the results together. You need to be on the same page when it comes to your budget and what’s realistic for your money situation. After all, shopping for your “home sweet home” will feel very unifying and exciting once you both have a shared vision.

To calculate how much home you can afford, simply follow these five steps.

1. Figure out 25% of your take-home pay.

To calculate how much house you can afford, use the 25% rule: Never spend more than 25% of your monthly take-home pay (after tax) on monthly mortgage payments. Following this rule keeps you safe from buying too much house and ending up house poor. I want your home to be a blessing, not a curse.

Let’s say you earn $5,000 a month (after taxes). According to the 25% rule I mentioned, that means your monthly house payment should be no more than $1,250. (That includes the principal, property taxes, HOA fees, etc.)

Stick to that number and you’ll have plenty of room in your budget to tackle other financial goals, like investing for retirement or saving for your kid’s college.

2. Use our mortgage calculator to determine your home budget.

Sure, you could crunch the numbers yourself by dividing a home price by 180 months (that's a 15-year mortgage) and then multiplying the decreasing monthly principal balance by your interest rate. But if you're anything like me, you probably broke a sweat just reading that formula.

See how much house you can afford with our free mortgage calculator!

To save yourself the time and headache of doing a ton of math, use our handy-dandy mortgage calculator.

Remember: This is just a ballpark figure! Don’t forget that grown-up stuff like property taxes and home insurance will top off your monthly payment with another few hundred dollars or so. If your down payment is less than 20%, you’ll need to add private mortgage insurance (PMI) fees to your monthly payment too (we’ll explain that more later). And if you’re looking at a home that’s part of a homeowners association (HOA), you’ll need to factor in those lovely fees as well.

I know that sounds like a lot to keep track of, so let’s look at an example. If you use our mortgage calculator and plug in a home value of $198,000 with a 20% down payment at a 5% interest rate, you’ll find that your maximum monthly payment of $1,250 jumps to $1,506 when you add in $182 for taxes and $71 for insurance. To get that number back down to a monthly housing budget of $1,250, you’ll need to lower the price of the house you can afford to $163,000.

Use our calculator to try out other combinations to find the right mortgage amount, interest rate and down payment combo that will work for your budget.

3. Don’t forget to factor in closing costs.

All right, don’t freak out here. But a down payment isn’t the only cash you’ll need to save up to buy a home. There are also closing costs to consider.

On average, closing costs are about 3–4% of the purchase price of your home.1 Your lender and real estate agent will let you know exactly how much your closing costs are so you can pay for them on closing day.

These costs cover important parts of the home-buying process, such as:

- Appraisal fees

- Home inspections

- Loan origination fees

- Credit reports

- Attorneys

- Home insurance

- Property taxes

Don’t forget to factor your closing costs into your overall home-buying budget. For example, if you’re purchasing a $200,000 home, multiply that by 4% and you’ll get an estimated closing cost of $8,000. Add that amount to your 20% down payment ($40,000), and the total cash you’ll need to purchase your home is $48,000.

If you don’t have the additional $8,000 for closing costs, you should hold off on your home purchase until you’ve saved up the extra cash or shoot a little lower on your home price range.

Whatever you do, don’t let the closing costs keep you from making the biggest down payment possible. The bigger the down payment, the less you’ll owe on your mortgage!

4. Consider homeownership costs.

Here’s the truth: Owning a home is expensive. Between repairs, upgrades and maintenance, those bills can add up. Your emergency fund of 3–6 months of expenses can cover major home disasters. But if you’re planning some home upgrades or you’re a first-time homeowner, add room in your monthly budget to cover unexpected expenses.

These costs can include:

- Increased utilities: On average, if you’re used to paying $100–150 on utilities as a renter in an apartment, you might need to bump up that budget closer to $400 a month as a homeowner.2

- Maintenance and repairs: Most homeowners spend about $3,200 a year on home maintenance projects.3 This could include things like landscaping or routine services like pest control and HVAC tune-ups.

- Upgrades and additions: Minor home upgrades can cost major bucks, so you’ll need to plan for that in your budget. For example, a minor kitchen remodel can cost over $26,000.4

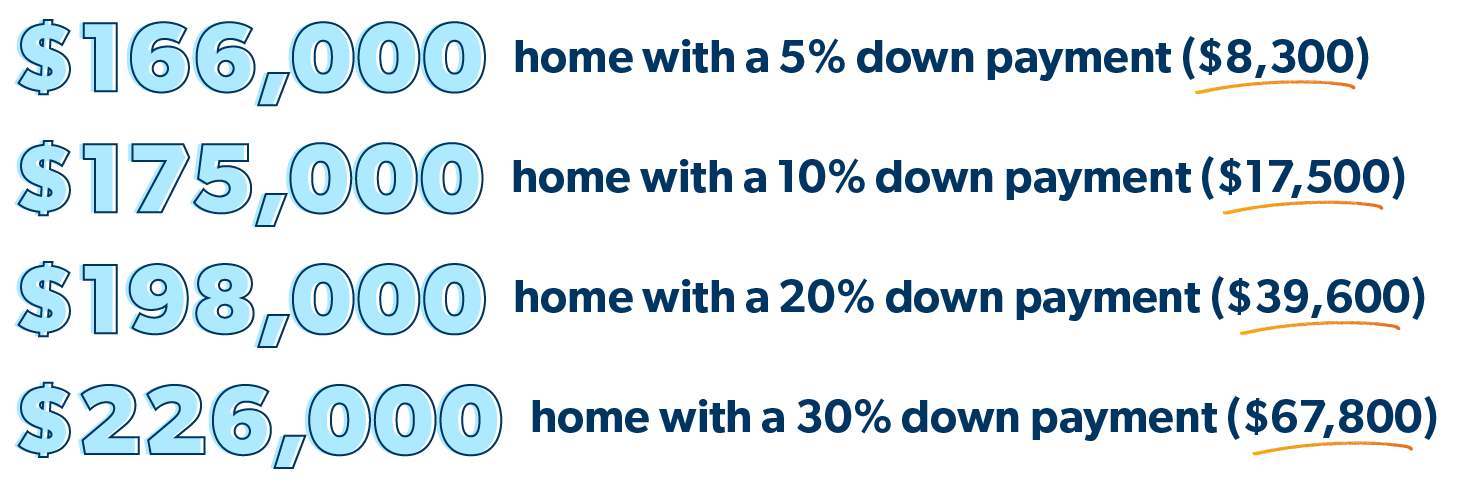

5. Save a bigger down payment to make your home more affordable.

Remember, your down payment makes a big impact on how much home you can afford. The more cash you put down, the less money you’ll need to borrow. That means lower mortgage payments each month and a faster timeline to pay off your home loan. Just imagine a home with zero payments!

Now, I’m always going to tell you the best way to buy a home is with 100% cash. But if saving up to pay cash isn’t reasonable for your timeline, you’ll probably get a mortgage. That’s okay! Just save up a down payment that’s 20% or more of the home price. If you’re a first-time home buyer, a down payment of 5–10% is okay—but you’ll have to pay that pesky private mortgage insurance (PMI).

PMI is a yearly fee that usually costs 1% of the total loan value. It’s another expense on top of your monthly payment. (Boo!) It protects the mortgage company in case you don’t make your payments and they have to take back the house (aka the dreaded foreclosure).

PMI might change how much house you can afford, so include it in your calculations if your down payment is less than 20%. If that’s you, stick to a 15-year fixed-rate mortgage with a monthly payment no more than 25% of your monthly take-home pay. (The rules don’t change!) You can also adjust your home price range to a lower amount so you can put down at least 20% in cash.

Trust me. It’s worth taking the extra time to save for a big down payment. Otherwise, you’ll be suffocating under a budget-crushing mortgage and paying thousands more in interest and fees.

How Much House Can I Afford Based on My Salary?

To calculate how much house you can afford, use the 25% rule—never spend more than 25% of your monthly take-home pay (after tax) on monthly mortgage payments.

That 25% limit includes principal, interest, property taxes, home insurance, PMI and don’t forget to consider HOA fees. Whoa—those are a lot of variables!

To figure out how much you can afford, simply take your monthly take-home pay and divide it by four. For example, if your take-home pay is $5,000 and you divide it by four, you’ll get $1,250.

Know Which Mortgage Option Is Right for You

Whew! That math wasn’t too bad, was it? Now let’s talk about different types of mortgages. Most of them (ARM, FHA, VA, USDA) are terrible because they’re designed to get you into a house even if you can’t afford it. They might look tempting but stay far away!

If you crunch the numbers, you’ll realize these mortgages charge you tens of thousands of dollars more in interest and fees. Meaning, you’ll pay way more over the life of the loan than you should.

That’s why getting the right mortgage is so important. Setting boundaries on the front end of your home-buying process makes it easier to find a house you love and that’s in your budget.

Here are the mortgage guidelines I recommend:

- A fixed-rate conventional loan: With this option, your interest rate never changes during the life of the loan. This keeps you protected from the rising rates of an adjustable-rate loan.

- A 15-year term: Your monthly payment will be higher with a 15-year term, but you’ll pay off your mortgage in half the time of a 30-year term . . . saving tens of thousands in interest.

Your mortgage lender will probably approve you for a bigger mortgage than you can afford. Don’t let your lender decide your home-buying budget. I repeat: Don’t let your lender decide your budget! Ignore the bank’s numbers and stick with your own.

Knowing your house budget and sticking to it is the only way to make sure you get a mortgage you can pay off as fast as possible.

How Will My Debt-to-Income Ratio Affect Affordability?

When you apply for a mortgage, lenders usually look at your debt-to-income ratio (DTI)— this is your total monthly debt payments divided by your gross monthly income (before tax) written as a percentage.

Lenders often use the 28/36 rule as a sign of a healthy DTI—meaning you won’t spend more than 28% of your gross monthly income on mortgage payments and no more than 36% of your income on total debt payments (including a mortgage, student loans, car loans and credit card debt).

If your DTI ratio is higher than the 28/36 rule, some lenders will still approve you for a loan. But they’ll charge you higher interest rates and add extra fees like mortgage insurance to protect themselves (not you) in case you get in over your head and can’t make your mortgage payments.

How Much House Does Dave Ramsey Say I Can Afford?

For decades, Dave Ramsey has told radio listeners to follow the 25% rule when buying a house—remember, that means never buying a house with a monthly payment that’s more than 25% of your monthly take-home pay on a 15-year fixed-rate conventional mortgage.

At Ramsey Solutions, we also teach people they can’t afford to buy a house until they:

- Are completely debt-free

- Have an emergency fund of 3–6 months of expenses

- Have a down payment of 20% or more (5–10% is okay for first-time home buyers)

Why is all this important? Because when life happens, an unexpected expense or a job loss could crush someone financially if they’re also trying to get out of debt and pay a mortgage. We don’t want that to happen to you.

What Salary Do You Need to Buy a $400,000 House?

Now let’s take what we’ve learned and put it into an example. Let’s say you want to buy a $400,000 house. First, you’ll need to do the hard work of saving up $80,000 in cash as a 20% down payment. Or if you already own a home, make sure you have enough equity to pay off your current mortgage and cover your down payment when you sell it.

With a 15-year mortgage at a 5% interest rate, your monthly payment would be around $2,500 (that’s only principal and interest). To cover that payment, you’d need to earn a monthly take-home pay of at least $10,000 ($2,500 is 25% of $10,000).

So, to buy a $400,000 home, your annual take-home salary would have to be more than $120,000 ($10,000 x 12 months). But you’d actually need more than that after adding in the cost of property taxes and home insurance.

If that doesn’t sound like you, don’t worry. You have a few options. You could save a bigger down payment to lower your monthly mortgage until it’s no more than 25% of your take-home pay. Or look for a smaller starter home in a more affordable neighborhood.

Work With a Buyer’s Agent We Trust

For more guidance on buying a house you can afford, work with a real estate agent. A good agent will help you set the right expectations when shopping for a home in your price range—they may even be able to find you a home for sale that other buyers don’t know about.

For a quick and easy way to find a RamseyTrusted agent, try our Endorsed Local Providers (ELP) program. We only recommend agents who truly care about your financial path and won’t push you to overspend on a house so they can bring home a bigger commission check. Find your real estate agent today!

Next Steps

- Write down your household's monthly take-home pay.

- Multiply it by 25%.

- Use a mortgage calculator to see you can change your home-buying budget.

Frequently Asked Questions

-

How do I budget for a house?

-

The first step to budgeting for a house is to know how much down payment you need. Ideally, you’ll want to save a down payment of at least 20%. For first-time home buyers, a smaller down payment like 5–10% is okay too—but then you’ll have to pay PMI. Whatever you do, never buy a house with a monthly payment that’s more than 25% of your monthly take-home pay on a 15-year fixed-rate mortgage (which has the overall lowest total cost). And stay away from expensive loans like FHA, VA and USDA.

After you’ve set your savings goal, here are some tips on how to save for a house: Pay off all your debt, tighten your spending, hold off on your retirement savings (temporarily), start a side job, and sell stuff you don’t need.

Let’s say you want to buy a $200,000 house. Your down payment savings goal is $40,000 (or 20% of the home price). To budget for this house in two years, you’d need to set aside close to $1,700 each month ($40,000 / 24 months = $1,670).

-

Where should I stash my down payment?

-

You can stash your down payment in a simple money market account or high-yield savings account. You won’t make tons on interest, but you won’t lose money either. But guys, don’t forget that saving a down payment is not the same as investing for retirement—you want to keep your savings liquid and in a place that’s easy to access.

-

When should I start saving for a house?

-

As soon as you’re debt-free with a full emergency fund of 3–6 months of your typical expenses, you’re ready to start saving for a house!

-

How can I save for a house quickly?

-

If you want to save for a house fast, you need to be debt-free and have an emergency fund of 3–6 months of expenses saved. With your income freed up from debt payments and an emergency fund to protect you from life’s unexpected surprises, you can save for a house much faster. Here are some other ideas to help you save money fast.

-

I can’t afford a house—what do I do?

-

Trying to buy a house when home prices are high can be really frustrating. But with the right plan, you can do it. Set a down payment goal and save like crazy for a year or two. Try these smart ways to save for a home down payment.

Once you have a strong down payment saved up, work with an experienced real estate agent who knows your area. The best agents will work hard to find you a house that fits your budget.

Did you find this article helpful? Share it!

About the author

Rachel Cruze